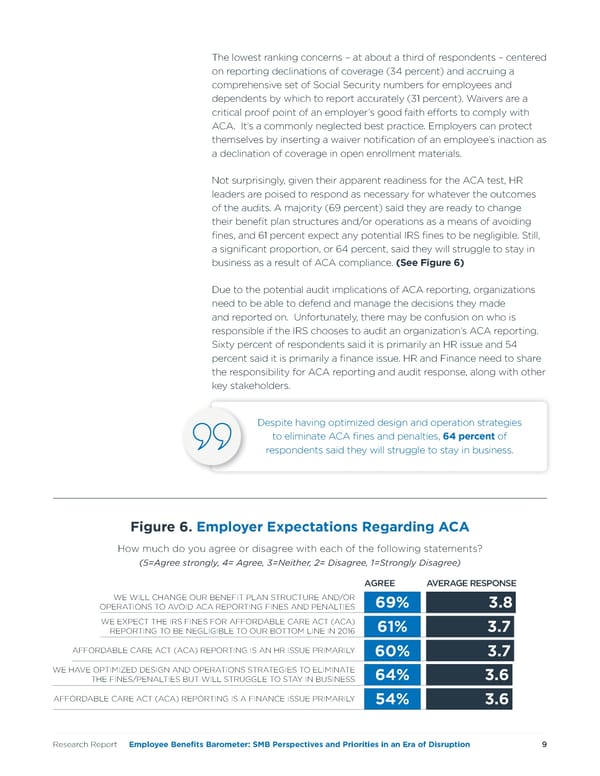

The lowest ranking concerns – at about a third of respondents – centered on reporting declinations of coverage (34 percent) and accruing a comprehensive set of Social Security numbers for employees and dependents by which to report accurately (31 percent). Waivers are a critical proof point of an employer’s good faith efforts to comply with ACA. It’s a commonly neglected best practice. Employers can protect themselves by inserting a waiver notification of an employee’s inaction as a declination of coverage in open enrollment materials. Not surprisingly, given their apparent readiness for the ACA test, HR leaders are poised to respond as necessary for whatever the outcomes of the audits. A majority (69 percent) said they are ready to change their benefit plan structures and/or operations as a means of avoiding fines, and 61 percent expect any potential IRS fines to be negligible. Still, a significant proportion, or 64 percent, said they will struggle to stay in business as a result of ACA compliance. (See Figure 6) Due to the potential audit implications of ACA reporting, organizations need to be able to defend and manage the decisions they made and reported on. Unfortunately, there may be confusion on who is responsible if the IRS chooses to audit an organization’s ACA reporting. Sixty percent of respondents said it is primarily an HR issue and 54 percent said it is primarily a finance issue. HR and Finance need to share the responsibility for ACA reporting and audit response, along with other key stakeholders. Despite having optimized design and operation strategies to eliminate ACA fines and penalties, 64 percent of respondents said they will struggle to stay in business. Figure 6. Employer Expectations Regarding ACA How much do you agree or disagree with each of the following statements? (5=Agree strongly, 4= Agree, 3=Neither, 2= Disagree, 1=Strongly Disagree) AGREE AVERAGE RESPONSE WE WILL CHANGE OUR BENEFIT PLAN STRUCTURE AND/OR 69% 3.8 OPERATIONS TO AVOID ACA REPORTING FINES AND PENALTIES WE EXPECT THE IRS FINES FOR AFFORDABLE CARE ACT (ACA) 61% 3.7 REPORTING TO BE NEGLIGIBLE TO OUR BOTTOM LINE IN 2016 AFFORDABLE CARE ACT (ACA) REPORTING IS AN HR ISSUE PRIMARILY 60% 3.7 WE HAVE OPTIMIZED DESIGN AND OPERATIONS STRATEGIES TO ELIMINATE 64% 3.6 THE FINES/PENALTIES BUT WILL STRUGGLE TO STAY IN BUSINESS AFFORDABLE CARE ACT (ACA) REPORTING IS A FINANCE ISSUE PRIMARILY 54% 3.6 Research Report | Employee Benefits Barometer: SMB Perspectives and Priorities in an Era of Disruption 9

Employee Benefits Barometer: SMB Perspectives and Priorities in an Era of Disruption Page 8 Page 10

Employee Benefits Barometer: SMB Perspectives and Priorities in an Era of Disruption Page 8 Page 10