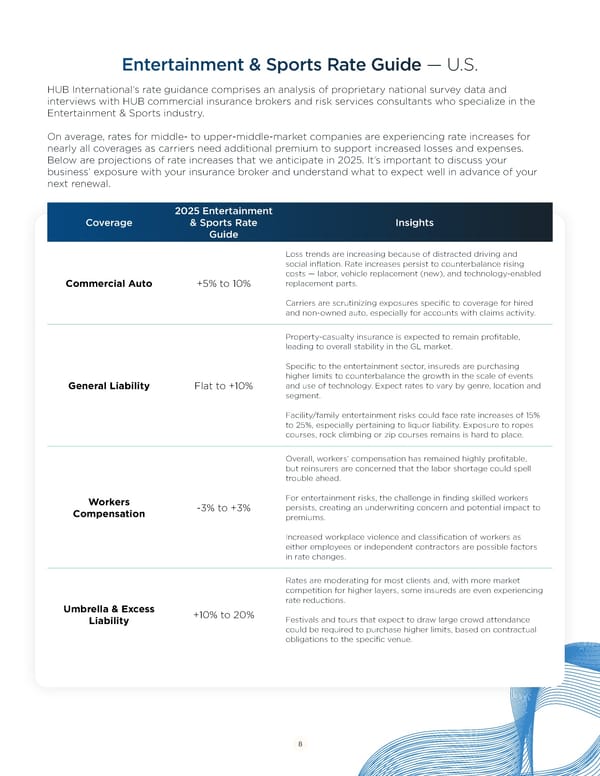

Entertainment & Sports Rate Guide — U.S. HUB International’s rate guidance comprises an analysis of proprietary national survey data and interviews with HUB commercial insurance brokers and risk services consultants who specialize in the Entertainment & Sports industry. On average, rates for middle- to upper-middle-market companies are experiencing rate increases for nearly all coverages as carriers need additional premium to support increased losses and expenses. Below are projections of rate increases that we anticipate in 2025. It’s important to discuss your business’ exposure with your insurance broker and understand what to expect well in advance of your next renewal. 2025 Entertainment Coverage & Sports Rate Insights Guide Loss trends are increasing because of distracted driving and social inflation. Rate increases persist to counterbalance rising costs — labor, vehicle replacement (new), and technology-enabled Commercial Auto +5% to 10% replacement parts. Carriers are scrutinizing exposures specific to coverage for hired and non-owned auto, especially for accounts with claims activity. Property-casualty insurance is expected to remain profitable, leading to overall stability in the GL market. Specific to the entertainment sector, insureds are purchasing higher limits to counterbalance the growth in the scale of events General Liability Flat to +10% and use of technology. Expect rates to vary by genre, location and segment. Facility/family entertainment risks could face rate increases of 15% to 25%, especially pertaining to liquor liability. Exposure to ropes courses, rock climbing or zip courses remains is hard to place. Overall, workers’ compensation has remained highly profitable, but reinsurers are concerned that the labor shortage could spell trouble ahead. Workers For entertainment risks, the challenge in finding skilled workers Compensation -3% to +3% persists, creating an underwriting concern and potential impact to premiums. Increased workplace violence and classification of workers as either employees or independent contractors are possible factors in rate changes. Rates are moderating for most clients and, with more market competition for higher layers, some insureds are even experiencing rate reductions. Umbrella & Excess +10% to 20% Liability Festivals and tours that expect to draw large crowd attendance could be required to purchase higher limits, based on contractual obligations to the specific venue. 8

Entertainment & Sports Risk Management Guide 2025 Page 7 Page 9

Entertainment & Sports Risk Management Guide 2025 Page 7 Page 9