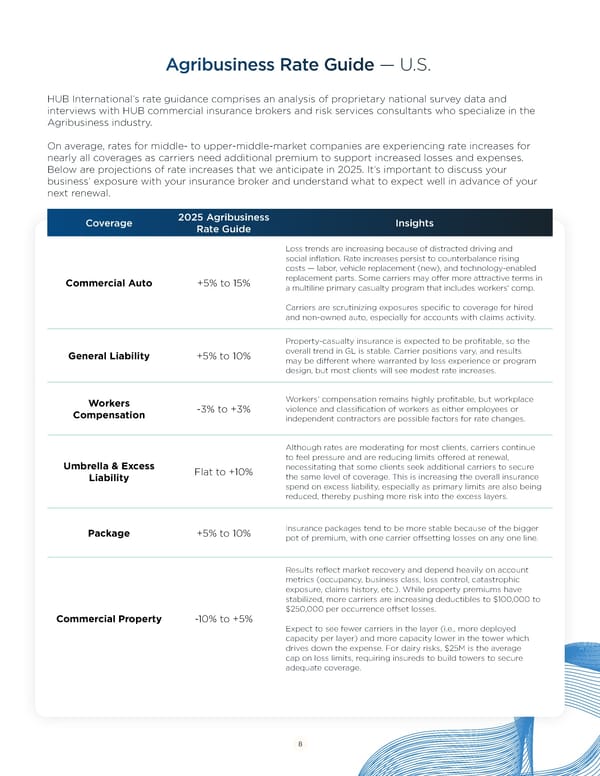

Agribusiness Rate Guide — U.S. HUB International’s rate guidance comprises an analysis of proprietary national survey data and interviews with HUB commercial insurance brokers and risk services consultants who specialize in the Agribusiness industry. On average, rates for middle- to upper-middle-market companies are experiencing rate increases for nearly all coverages as carriers need additional premium to support increased losses and expenses. Below are projections of rate increases that we anticipate in 2025. It’s important to discuss your business’ exposure with your insurance broker and understand what to expect well in advance of your next renewal. Coverage 2025 Agribusiness Insights Rate Guide Loss trends are increasing because of distracted driving and social inflation. Rate increases persist to counterbalance rising costs — labor, vehicle replacement (new), and technology-enabled Commercial Auto +5% to 15% replacement parts. Some carriers may offer more attractive terms in a multiline primary casualty program that includes workers' comp. Carriers are scrutinizing exposures specific to coverage for hired and non-owned auto, especially for accounts with claims activity. Property-casualty insurance is expected to be profitable, so the General Liability +5% to 10% overall trend in GL is stable. Carrier positions vary, and results may be different where warranted by loss experience or program design, but most clients will see modest rate increases. Workers Workers’ compensation remains highly profitable, but workplace Compensation -3% to +3% violence and classification of workers as either employees or independent contractors are possible factors for rate changes. Although rates are moderating for most clients, carriers continue to feel pressure and are reducing limits offered at renewal, Umbrella & Excess Flat to +10% necessitating that some clients seek additional carriers to secure Liability the same level of coverage. This is increasing the overall insurance spend on excess liability, especially as primary limits are also being reduced, thereby pushing more risk into the excess layers. Package +5% to 10% Insurance packages tend to be more stable because of the bigger pot of premium, with one carrier offsetting losses on any one line. Results reflect market recovery and depend heavily on account metrics (occupancy, business class, loss control, catastrophic exposure, claims history, etc.). While property premiums have stabilized, more carriers are increasing deductibles to $100,000 to $250,000 per occurrence offset losses. Commercial Property -10% to +5% Expect to see fewer carriers in the layer (i.e., more deployed capacity per layer) and more capacity lower in the tower which drives down the expense. For dairy risks, $25M is the average cap on loss limits, requiring insureds to build towers to secure adequate coverage. 8

Navigating Agribusiness Challenges in 2025 Page 7 Page 9

Navigating Agribusiness Challenges in 2025 Page 7 Page 9