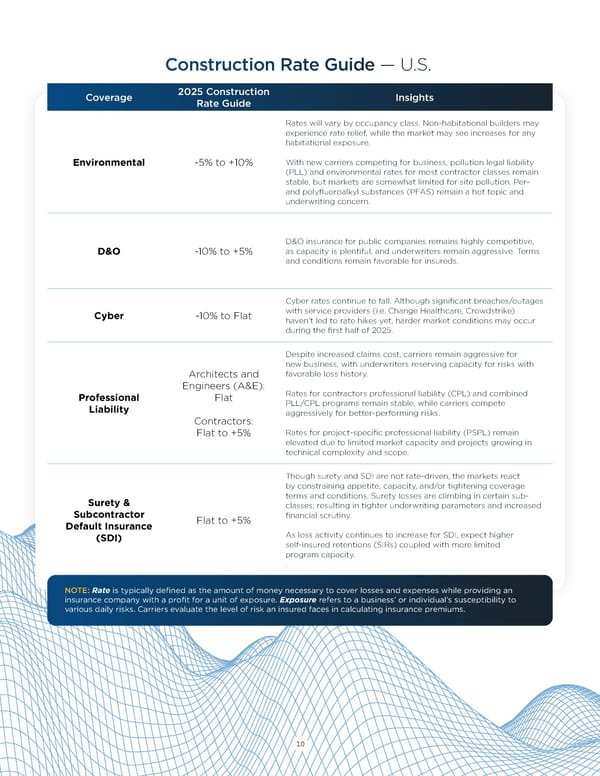

Construction Rate Guide — U.S. Coverage 2025 Construction Insights Rate Guide Rates will vary by occupancy class. Non-habitational builders may experience rate relief, while the market may see increases for any habitational exposure. Environmental -5% to +10% With new carriers competing for business, pollution legal liability (PLL) and environmental rates for most contractor classes remain stable, but markets are somewhat limited for site pollution. Per- and polyfluoroalkyl substances (PFAS) remain a hot topic and underwriting concern. D&O insurance for public companies remains highly competitive, D&O -10% to +5% as capacity is plentiful, and underwriters remain aggressive. Terms and conditions remain favorable for insureds. Cyber rates continue to fall. Although significant breaches/outages Cyber -10% to Flat with service providers (i.e. Change Healthcare, Crowdstrike) haven’t led to rate hikes yet, harder market conditions may occur during the first half of 2025. Despite increased claims cost, carriers remain aggressive for new business, with underwriters reserving capacity for risks with Architects and favorable loss history. Engineers (A&E): Professional Flat Rates for contractors professional liability (CPL) and combined Liability PLL/CPL programs remain stable, while carriers compete Contractors: aggressively for better-performing risks. Flat to +5% Rates for project-specific professional liability (PSPL) remain elevated due to limited market capacity and projects growing in technical complexity and scope. Though surety and SDI are not rate-driven, the markets react by constraining appetite, capacity, and/or tightening coverage Surety & terms and conditions. Surety losses are climbing in certain sub- classes, resulting in tighter underwriting parameters and increased Subcontractor Flat to +5% financial scrutiny. Default Insurance (SDI) As loss activity continues to increase for SDI, expect higher self-insured retentions (SIRs) coupled with more limited program capacity. . NOTE: Rate is typically defined as the amount of money necessary to cover losses and expenses while providing an insurance company with a profit for a unit of exposure. Exposure refers to a business’ or individual’s susceptibility to various daily risks. Carriers evaluate the level of risk an insured faces in calculating insurance premiums. 10

Navigating Construction Risks and Opportunities in 2025 Page 9 Page 11

Navigating Construction Risks and Opportunities in 2025 Page 9 Page 11