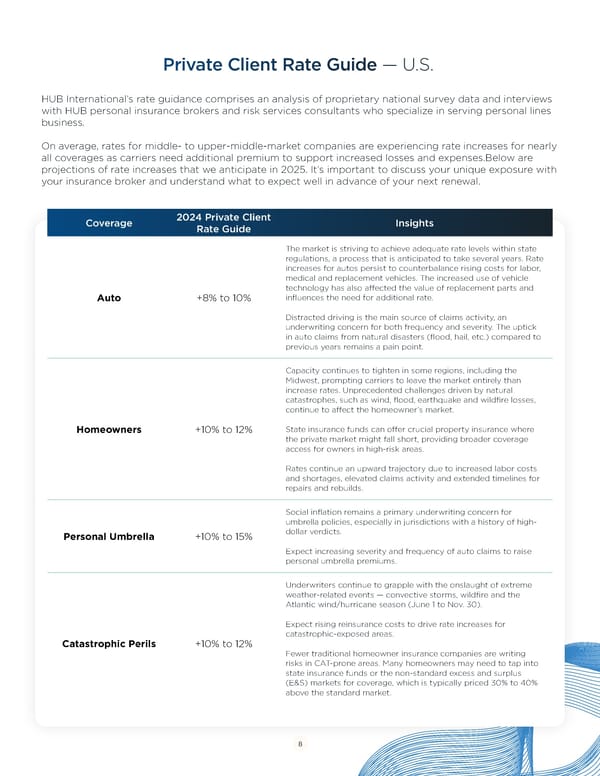

Private Client Rate Guide — U.S. HUB International’s rate guidance comprises an analysis of proprietary national survey data and interviews with HUB personal insurance brokers and risk services consultants who specialize in serving personal lines business. On average, rates for middle- to upper-middle-market companies are experiencing rate increases for nearly all coverages as carriers need additional premium to support increased losses and expenses.Below are projections of rate increases that we anticipate in 2025. It’s important to discuss your unique exposure with your insurance broker and understand what to expect well in advance of your next renewal. Coverage 2024 Private Client Insights Rate Guide The market is striving to achieve adequate rate levels within state regulations, a process that is anticipated to take several years. Rate increases for autos persist to counterbalance rising costs for labor, medical and replacement vehicles. The increased use of vehicle technology has also affected the value of replacement parts and Auto +8% to 10% influences the need for additional rate. Distracted driving is the main source of claims activity, an underwriting concern for both frequency and severity. The uptick in auto claims from natural disasters (flood, hail, etc.) compared to previous years remains a pain point. Capacity continues to tighten in some regions, including the Midwest, prompting carriers to leave the market entirely than increase rates. Unprecedented challenges driven by natural catastrophes, such as wind, flood, earthquake and wildfire losses, continue to affect the homeowner’s market. Homeowners +10% to 12% State insurance funds can offer crucial property insurance where the private market might fall short, providing broader coverage access for owners in high-risk areas. Rates continue an upward trajectory due to increased labor costs and shortages, elevated claims activity and extended timelines for repairs and rebuilds. Social inflation remains a primary underwriting concern for umbrella policies, especially in jurisdictions with a history of high- Personal Umbrella +10% to 15% dollar verdicts. Expect increasing severity and frequency of auto claims to raise personal umbrella premiums. Underwriters continue to grapple with the onslaught of extreme weather-related events — convective storms, wildfire and the Atlantic wind/hurricane season (June 1 to Nov. 30). Expect rising reinsurance costs to drive rate increases for catastrophic-exposed areas. Catastrophic Perils +10% to 12% Fewer traditional homeowner insurance companies are writing risks in CAT-prone areas. Many homeowners may need to tap into state insurance funds or the non-standard excess and surplus (E&S) markets for coverage, which is typically priced 30% to 40% above the standard market. 88

Navigating Risk in 2025: Protecting High-Value Assets and Estates Page 7 Page 9

Navigating Risk in 2025: Protecting High-Value Assets and Estates Page 7 Page 9