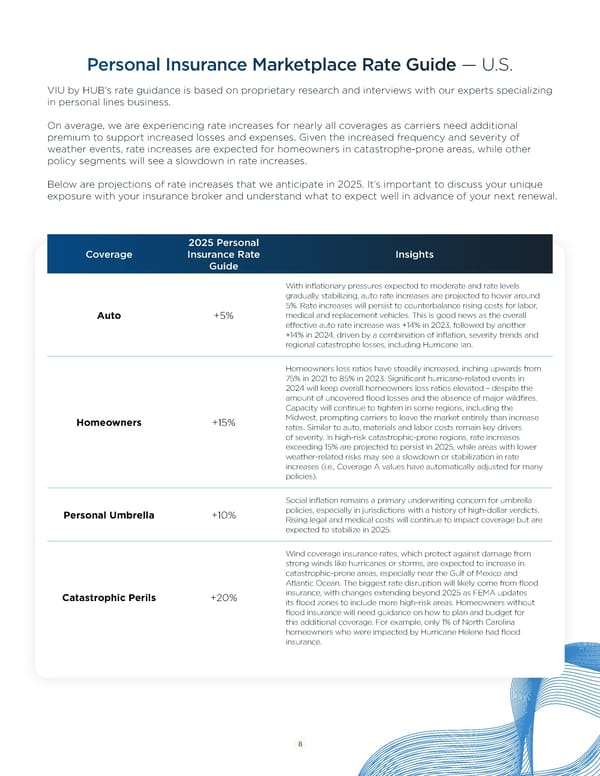

Personal Insurance Marketplace Rate Guide — U.S. VIU by HUB's rate guidance is based on proprietary research and interviews with our experts specializing in personal lines business. On average, we are experiencing rate increases for nearly all coverages as carriers need additional premium to support increased losses and expenses. Given the increased frequency and severity of weather events, rate increases are expected for homeowners in catastrophe-prone areas, while other policy segments will see a slowdown in rate increases. Below are projections of rate increases that we anticipate in 2025. It’s important to discuss your unique exposure with your insurance broker and understand what to expect well in advance of your next renewal. 2025 Personal Coverage Insurance Rate Insights Guide With inflationary pressures expected to moderate and rate levels gradually stabilizing, auto rate increases are projected to hover around 5%. Rate increases will persist to counterbalance rising costs for labor, Auto +5% medical and replacement vehicles. This is good news as the overall effective auto rate increase was +14% in 2023, followed by another +14% in 2024, driven by a combination of inflation, severity trends and regional catastrophe losses, including Hurricane Ian. Homeowners loss ratios have steadily increased, inching upwards from 75% in 2021 to 85% in 2023. Significant hurricane-related events in 2024 will keep overall homeowners loss ratios elevated – despite the amount of uncovered flood losses and the absence of major wildfires. Capacity will continue to tighten in some regions, including the Homeowners +15% Midwest, prompting carriers to leave the market entirely than increase rates. Similar to auto, materials and labor costs remain key drivers of severity. In high-risk catastrophic-prone regions, rate increases exceeding 15% are projected to persist in 2025, while areas with lower weather-related risks may see a slowdown or stabilization in rate increases (i.e., Coverage A values have automatically adjusted for many policies). Social inflation remains a primary underwriting concern for umbrella Personal Umbrella +10% policies, especially in jurisdictions with a history of high-dollar verdicts. Rising legal and medical costs will continue to impact coverage but are expected to stabilize in 2025. Wind coverage insurance rates, which protect against damage from strong winds like hurricanes or storms, are expected to increase in catastrophic-prone areas, especially near the Gulf of Mexico and Atlantic Ocean. The biggest rate disruption will likely come from flood Catastrophic Perils +20% insurance, with changes extending beyond 2025 as FEMA updates its flood zones to include more high-risk areas. Homeowners without flood insurance will need guidance on how to plan and budget for this additional coverage. For example, only 1% of North Carolina homeowners who were impacted by Hurricane Helene had flood insurance. 8

Personal Insurance Trends & Partnership Strategies for 2025 Page 7 Page 9

Personal Insurance Trends & Partnership Strategies for 2025 Page 7 Page 9