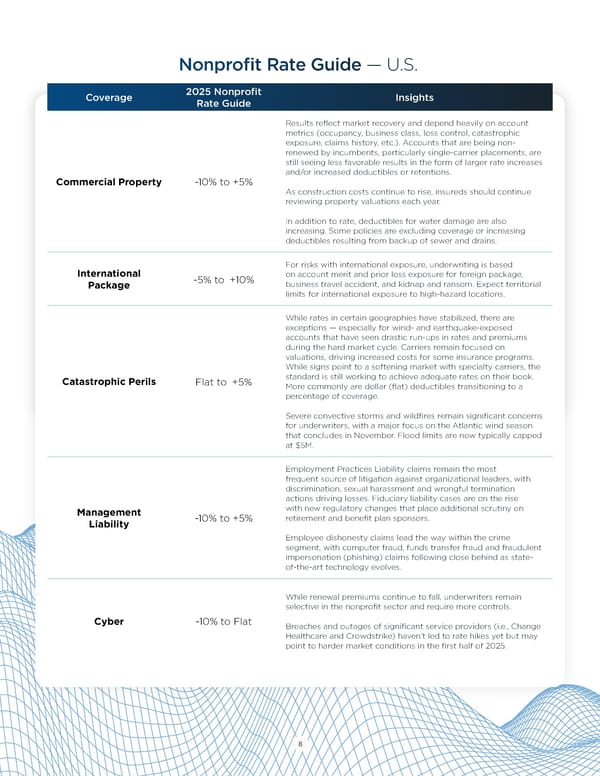

Nonprofit Rate Guide — U.S. 2025 Nonprofit Coverage 2024 Rate Guide Insights Coverage Rate Guide Insights Empor am res denietur ra veriae voloreceriam aut ad ut Results reflect market recovery and depend heavily on account asperch iciunt, quiae nonseque plab ipsam se este int etur metrics (occupancy, business class, loss control, catastrophic sum voluptatemos sit eliquibeaquo eum exceremped etur sum exposure, claims history, etc.). Accounts that are being non- Lorem ipsum -0% to +0% inverio nsequib usandit qui conecto cus rem quatur sectiatem renewed by incumbents, particularly single-carrier placements, are illant evel minture qui res perfereped qui corehen istiati squibea still seeing less favorable results in the form of larger rate increases tescipsunti occus re es dolorer ferspietur, sunda volecer namende and/or increased deductibles or retentions. Commercial Property -10% to +5% sandae. Ecus maion conseni taquiae rferro doluptiat volorem qui comnisquas restrumet. As construction costs continue to rise, insureds should continue reviewing property valuations each year. Empor am res denietur ra veriae voloreceriam aut ad ut asperch iciunt, quiae nonseque plab ipsam se este int etur In addition to rate, deductibles for water damage are also sum voluptatemos sit eliquibeaquo eum exceremped etur sum increasing. Some policies are excluding coverage or increasing inverio nsequib usandit qui conecto cus rem quatur sectiatem Lorem ipsum -0% to +0% deductibles resulting from backup of sewer and drains. illant evel minture qui res perfereped qui corehen istiati squibea tescipsunti occus re es dolorer ferspietur, sunda volecer namende For risks with international exposure, underwriting is based International sandae. Ecus maion conseni taquiae rferro doluptiat volorem qui on account merit and prior loss exposure for foreign package, -5% to +10% comnisquas restrumet. Package business travel accident, and kidnap and ransom. Expect territorial limits for international exposure to high-hazard locations. Empor am res denietur ra veriae voloreceriam aut ad ut asperch iciunt, quiae nonseque plab ipsam se este int etur While rates in certain geographies have stabilized, there are sum voluptatemos sit eliquibeaquo eum exceremped etur sum exceptions — especially for wind- and earthquake-exposed Lorem ipsum -0% to +0% inverio nsequib usandit qui conecto cus rem quatur sectiatem accounts that have seen drastic run-ups in rates and premiums illant evel minture qui res perfereped qui corehen istiati squibea during the hard market cycle. Carriers remain focused on tescipsunti occus re es dolorer ferspietur, sunda volecer namende valuations, driving increased costs for some insurance programs. sandae. Ecus maion conseni taquiae rferro doluptiat volorem qui While signs point to a softening market with specialty carriers, the comnisquas restrumet. Catastrophic Perils Flat to +5% standard is still working to achieve adequate rates on their book. More commonly are dollar (flat) deductibles transitioning to a percentage of coverage. NOTE: Rate is typically defined as the amount of money necessary to cover losses, expenses, and provide an insurance company with a profit for a unit of exposure. Exposure refers to a business’ or individual’s susceptibility to various risks Severe convective storms and wildfires remain significant concerns encountered daily. Carriers evaluate the level of risk an insured faces in calculating insurance premiums. for underwriters, with a major focus on the Atlantic wind season that concludes in November. Flood limits are now typically capped at $5M. Employment Practices Liability claims remain the most frequent source of litigation against organizational leaders, with discrimination, sexual harassment and wrongful termination actions driving losses. Fiduciary liability cases are on the rise Management with new regulatory changes that place additional scrutiny on Liability -10% to +5% retirement and benefit plan sponsors. Employee dishonesty claims lead the way within the crime segment, with computer fraud, funds transfer fraud and fraudulent impersonation (phishing) claims following close behind as state- of-the-art technology evolves. While renewal premiums continue to fall, underwriters remain selective in the nonprofit sector and require more controls. Cyber -10% to Flat Breaches and outages of significant service providers (i.e., Change Healthcare and Crowdstrike) haven’t led to rate hikes yet but may point to harder market conditions in the first half of 2025. 8

Building Nonprofit Resilience: 2025 Market Guide Page 7 Page 9

Building Nonprofit Resilience: 2025 Market Guide Page 7 Page 9