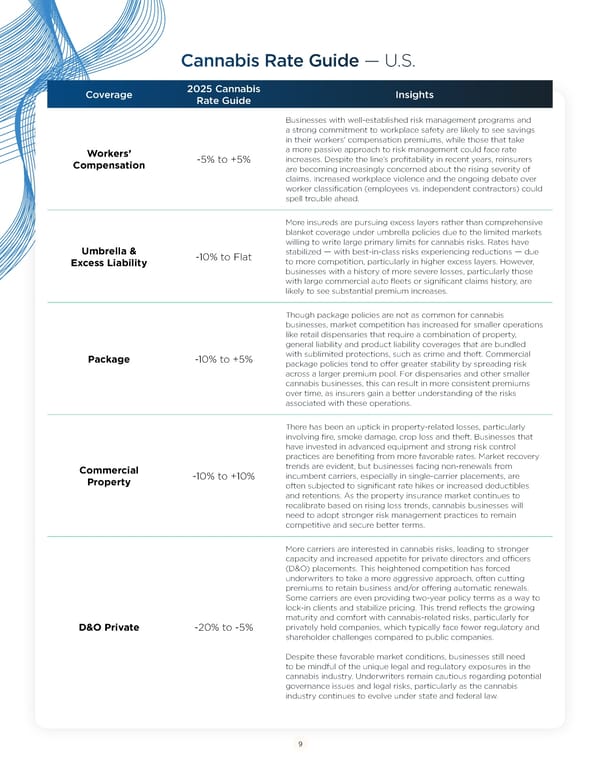

Cannabis Rate Guide — U.S. Coverage 2025 Cannabis Insights Rate Guide Businesses with well-established risk management programs and a strong commitment to workplace safety are likely to see savings in their workers' compensation premiums, while those that take Workers’ a more passive approach to risk management could face rate Compensation -5% to +5% increases. Despite the line’s profitability in recent years, reinsurers are becoming increasingly concerned about the rising severity of claims. Increased workplace violence and the ongoing debate over worker classification (employees vs. independent contractors) could spell trouble ahead. More insureds are pursuing excess layers rather than comprehensive blanket coverage under umbrella policies due to the limited markets willing to write large primary limits for cannabis risks. Rates have Umbrella & -10% to Flat stabilized — with best-in-class risks experiencing reductions — due Excess Liability to more competition, particularly in higher excess layers. However, businesses with a history of more severe losses, particularly those with large commercial auto fleets or significant claims history, are likely to see substantial premium increases. Though package policies are not as common for cannabis businesses, market competition has increased for smaller operations like retail dispensaries that require a combination of property, general liability and product liability coverages that are bundled Package -10% to +5% with sublimited protections, such as crime and theft. Commercial package policies tend to offer greater stability by spreading risk across a larger premium pool. For dispensaries and other smaller cannabis businesses, this can result in more consistent premiums over time, as insurers gain a better understanding of the risks associated with these operations. There has been an uptick in property-related losses, particularly involving fire, smoke damage, crop loss and theft. Businesses that have invested in advanced equipment and strong risk control practices are benefiting from more favorable rates. Market recovery Commercial trends are evident, but businesses facing non-renewals from Property -10% to +10% incumbent carriers, especially in single-carrier placements, are often subjected to significant rate hikes or increased deductibles and retentions. As the property insurance market continues to recalibrate based on rising loss trends, cannabis businesses will need to adopt stronger risk management practices to remain competitive and secure better terms. More carriers are interested in cannabis risks, leading to stronger capacity and increased appetite for private directors and ofÏcers (D&O) placements. This heightened competition has forced underwriters to take a more aggressive approach, often cutting premiums to retain business and/or offering automatic renewals. Some carriers are even providing two-year policy terms as a way to lock-in clients and stabilize pricing. This trend reflects the growing maturity and comfort with cannabis-related risks, particularly for D&O Private -20% to -5% privately held companies, which typically face fewer regulatory and shareholder challenges compared to public companies. Despite these favorable market conditions, businesses still need to be mindful of the unique legal and regulatory exposures in the cannabis industry. Underwriters remain cautious regarding potential governance issues and legal risks, particularly as the cannabis industry continues to evolve under state and federal law. 9

Cannabis Industry Risk & Resilience: Strategies for 2025 Page 8 Page 10

Cannabis Industry Risk & Resilience: Strategies for 2025 Page 8 Page 10