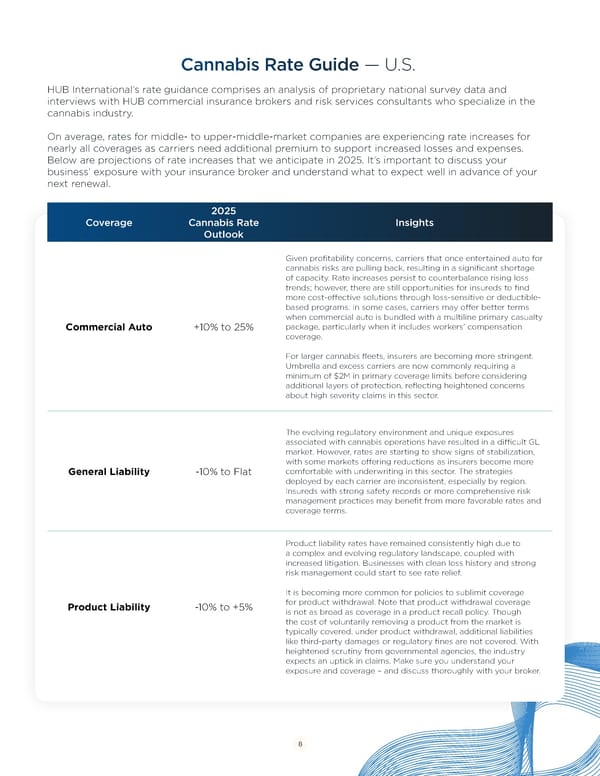

Cannabis Rate Guide — U.S. HUB International’s rate guidance comprises an analysis of proprietary national survey data and interviews with HUB commercial insurance brokers and risk services consultants who specialize in the cannabis industry. On average, rates for middle- to upper-middle-market companies are experiencing rate increases for nearly all coverages as carriers need additional premium to support increased losses and expenses. Below are projections of rate increases that we anticipate in 2025. It’s important to discuss your business’ exposure with your insurance broker and understand what to expect well in advance of your next renewal. 2025 Coverage Cannabis Rate Insights Outlook Given profitability concerns, carriers that once entertained auto for cannabis risks are pulling back, resulting in a significant shortage of capacity. Rate increases persist to counterbalance rising loss trends; however, there are still opportunities for insureds to find more cost-effective solutions through loss-sensitive or deductible- based programs. In some cases, carriers may offer better terms when commercial auto is bundled with a multiline primary casualty Commercial Auto +10% to 25% package, particularly when it includes workers' compensation coverage. For larger cannabis fleets, insurers are becoming more stringent. Umbrella and excess carriers are now commonly requiring a minimum of $2M in primary coverage limits before considering additional layers of protection, reflecting heightened concerns about high severity claims in this sector. The evolving regulatory environment and unique exposures associated with cannabis operations have resulted in a difÏcult GL market. However, rates are starting to show signs of stabilization, with some markets offering reductions as insurers become more General Liability -10% to Flat comfortable with underwriting in this sector. The strategies deployed by each carrier are inconsistent, especially by region. Insureds with strong safety records or more comprehensive risk management practices may benefit from more favorable rates and coverage terms. Product liability rates have remained consistently high due to a complex and evolving regulatory landscape, coupled with increased litigation. Businesses with clean loss history and strong risk management could start to see rate relief. It is becoming more common for policies to sublimit coverage Product Liability -10% to +5% for product withdrawal. Note that product withdrawal coverage is not as broad as coverage in a product recall policy. Though the cost of voluntarily removing a product from the market is typically covered. under product withdrawal, additional liabilities like third-party damages or regulatory fines are not covered. With heightened scrutiny from governmental agencies, the industry expects an uptick in claims. Make sure you understand your exposure and coverage – and discuss thoroughly with your broker. 8

Cannabis Industry Risk & Resilience: Strategies for 2025 Page 7 Page 9

Cannabis Industry Risk & Resilience: Strategies for 2025 Page 7 Page 9