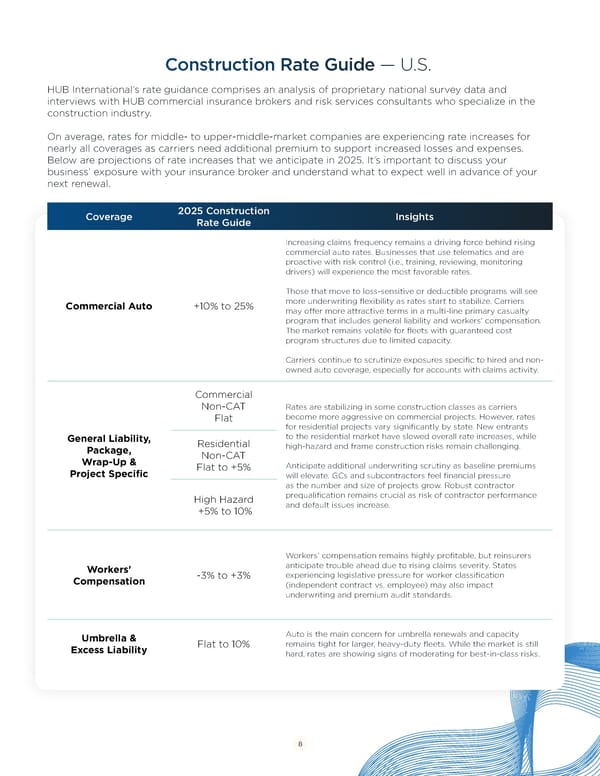

Construction Rate Guide — U.S. HUB International’s rate guidance comprises an analysis of proprietary national survey data and interviews with HUB commercial insurance brokers and risk services consultants who specialize in the construction industry. On average, rates for middle- to upper-middle-market companies are experiencing rate increases for nearly all coverages as carriers need additional premium to support increased losses and expenses. Below are projections of rate increases that we anticipate in 2025. It’s important to discuss your business’ exposure with your insurance broker and understand what to expect well in advance of your next renewal. Coverage 2025 Construction Insights Rate Guide Increasing claims frequency remains a driving force behind rising commercial auto rates. Businesses that use telematics and are proactive with risk control (i.e., training, reviewing, monitoring drivers) will experience the most favorable rates. Those that move to loss-sensitive or deductible programs will see Commercial Auto +10% to 25% more underwriting flexibility as rates start to stabilize. Carriers may offer more attractive terms in a multi-line primary casualty program that includes general liability and workers' compensation. The market remains volatile for fleets with guaranteed cost program structures due to limited capacity. Carriers continue to scrutinize exposures specific to hired and non- owned auto coverage, especially for accounts with claims activity. Commercial Non-CAT Rates are stabilizing in some construction classes as carriers Flat become more aggressive on commercial projects. However, rates for residential projects vary significantly by state. New entrants General Liability, Residential to the residential market have slowed overall rate increases, while Package, high-hazard and frame construction risks remain challenging. Wrap-Up & Non-CAT Project Specific Flat to +5% Anticipate additional underwriting scrutiny as baseline premiums will elevate. GCs and subcontractors feel financial pressure as the number and size of projects grow. Robust contractor High Hazard prequalification remains crucial as risk of contractor performance +5% to 10% and default issues increase. Workers’ compensation remains highly profitable, but reinsurers Workers' anticipate trouble ahead due to rising claims severity. States Compensation -3% to +3% experiencing legislative pressure for worker classification (independent contract vs. employee) may also impact underwriting and premium audit standards. Umbrella & Auto is the main concern for umbrella renewals and capacity Excess Liability Flat to 10% remains tight for larger, heavy-duty fleets. While the market is still hard, rates are showing signs of moderating for best-in-class risks. 8

Navigating Construction Risks and Opportunities in 2025 Page 7 Page 9

Navigating Construction Risks and Opportunities in 2025 Page 7 Page 9