Outlook 2025: North American Report

The "Outlook 2025: North American Report" provides strategic insights into risk management, insurance, and benefits strategies for businesses in North America. Published by HUB, the report covers key areas such as profitability, workforce vitality, and resilience, while identifying opportunities arising from disruptions.

North American Report Lean In. Seek Opportunity. Win Big. Optimize your Risk Management, Insurance and Benefits Strategies Risk & Insurance | Employee Benefits | Retirement & Private Wealth

Table of Contents Executive Summary and Key Insights 3 Profitability: Both New and Familiar Risks 7 Threaten Company Profits Workforce Vitality: Human Resources Leaders Grapple with 15 Employee Productivity and Rising Costs Resiliency: Getting Ready for the Next Major Disruption 22 Conclusion: Can Disruption Create New Opportunities? 26

Executive Summary and Key Insights Lean In. Seek Opportunity. Win Big. Optimize your Risk Management, Insurance and Benefits Strategies Today’s leaders face a business landscape that is more complex with risks that are highly interconnected. Alignment across the entire organization is key to preparing for and responding to economic, political, social and environmental challenges. A siloed approach to risk management leaves businesses vulnerable. The speed of change is dizzying, but those who embrace new approaches and solutions will improve their profitability, workplace vitality and resilience. 3 | HUB International 2025 North American Outlook Report

The HUB International 2025 Outlook Executive Survey The HUB International 2025 Outlook Executive Survey reports overall positive sentiment, but against this backdrop business leaders face major challenges to their profitability, employee productivity and company resilience, reflecting the inherent challenge of managing a constantly shifting risk environment. While the majority state that they are well prepared to address the impact of increased expenditures and economic uncertainty on their profits, they face greater uncertainty in preparing for climate change, natural disasters, cyber risks including deepfakes, increasing use of AI and geopolitical risk. We invite you to explore this year’s report and learn what your peers are thinking and doing to prepare for the year ahead. We surveyed 900 business leaders across the U.S. and Canada, representing 11 different industries and business segments, with the majority reporting revenues between $100 million and $1 billion. The respondents are leaders and decision-makers in corporate leadership, risk management and human resources at both public and private companies and nonprofit organizations.

Key Insights Siloed teams put businesses at risk. Organizations with integrated risk management and benefits best practices are better equipped to achieve sustained profitability, workforce vitality and resiliency. The HUB 2025 Outlook Executive Survey highlights that while risk and disruption will continue, successful business leaders are making constant shifts to navigate an increasingly complex world. With the right partners and analytic insights, they can gain an edge and remain resilient amid unforeseen disruption. The HUB 2025 Outlook Executive Survey reveals: • The overall sentiment for 2025 is predominantly positive, with 49% of surveyed companies reporting that they are highly confident and 33% cautiously optimistic about their company’s performance and prospects for 2025. • 68% of survey respondents expect revenue growth of up to 10% in 2025, while 36% of upper middle market companies1 anticipate growth between 10% and 50%. • 45% are planning or implementing strategic partnerships, 43% are planning or implementing M&A activities and 35% are planning international expansion. • 92% have a comprehensive employee benefits strategy. Slightly more than 40% are planning to make compensation adjustments on a market-by-market basis to address areas of concern. • AI is identified as a key priority most likely to positively impact profitability in 2025 by 35% of survey respondents, a 9% increase over 2023. While awareness of the power of AI has increased year over year, readiness to move forward remains at 53% among those who indicated it was a top priority. 1. Upper middle market companies are defined as those with revenues exceeding $1.5 billion. Middle Market = revenue from $100 million up to $1.5 billion. 5 | HUB International 2025 North American Outlook Report

Seize the Opportunity to Drive Impact Based on our survey findings, here are four key actions that organizations must consider to prepare for the future. Lean into insurance as a strategic tool and not a procurement exercise. 1 Risk exposures are increasing in complexity, frequency and severity. When it comes to insurance, don’t just set it and forget it. Insurance programs should be reviewed at least annually with an insurance broker and replacement costs and policy limits updated. Lean into data and analytics to power business strategy. Business leaders have gone from a “toe in the water” to a massive acceleration in the use of data and 2 analytics to manage insurance costs, enhance employee benefits and “to see around the corner.” Leading-edge organizations that use data and analytics possess greater insight into risk exposures, increase employee engagement and achieve greater alignment when it comes to decision-making. Lean into alternative risk transfer solutions. 3 When traditional insurance coverage isn’t available at an affordable cost, organizations need to explore other coverage options to protect their bottom line, company reputation and people. These alternative solutions may include captives and parametric insurance. Lean into risk management to build better resilience. 4 Organizations that integrate risk management into their corporate culture and overall business strategy are better equipped to navigate turbulence than their competitors. More importantly, such organizations gain the power to turn business disruption into opportunities for growth. 6 | HUB International North America 2025 Outlook Report HUB International 2025 North American Outlook Report | 6

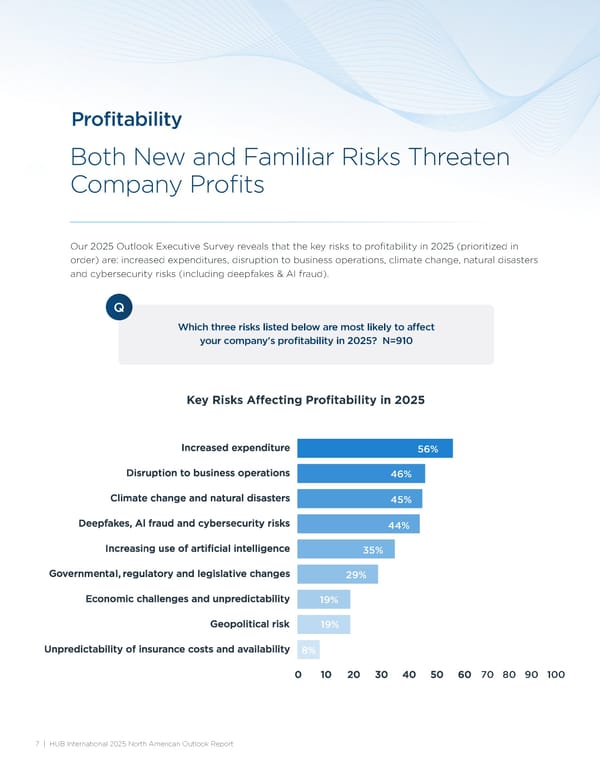

Profitability Both New and Familiar Risks Threaten Company Profits Our 2025 Outlook Executive Survey reveals that the key risks to profitability in 2025 (prioritized in order) are: increased expenditures, disruption to business operations, climate change, natural disasters and cybersecurity risks (including deepfakes & AI fraud). Q Which three risks listed below are most likely to affect your company's profitability in 2025? N=910 Key Risks Affecting Profitability in 2025 56% 46% 45% 44% 35% 29% 19% 19% 8% 70 80 90 100 hubinternational.com 7 | HUB International 2025 North American Outlook Report

While respondents report a high level of preparedness to manage the impact of increased expenditures and business disruption on profitability, they concede that they are less prepared to handle climate change and cyber risks. Canadian survey respondents expressed greater confidence in their preparedness to tackle key risks to profitability compared to their U.S. counterparts but rated themselves as less prepared to respond to climate change, AI adoption and regulatory changes. Q Of the profitability-related risks you selected, which risks is your company prepared to address today? N=910 Readiness to Tackle Risks and Mitigate Impact on Profitability 61% 50% 41% 44% 53% 37% 60% 31% 38% 80 90 100 HUB International 2025 North American Outlook Report | 8

Managing the Universal Threat of Climate Change The frequency and intensity of extreme weather impacts communities that just a few years ago were largely unaffected. Record-breaking floods, heatwaves, wildfires and storms are all becoming more recurrent and more intense. Severe convective storms are among the most common and most damaging natural catastrophes worldwide. The average annual loss from global natural catastrophes reached a new high of $151 billion (with non- 2 crop losses making up $119 billion). Global annual damages from climate change could reach $38 trillion 3 by 2050, mainly due to rising temperatures and changes in rainfall patterns and temperature variability. Planning for severe weather is crucial to building organizational resilience. Companies that can recover quickly from a catastrophic weather event are better positioned to enhance their brand reputation, support employees and differentiate themselves from competitors in their community. Here’s how your insurance broker can help you prepare for a major How Your Broker Can Help: Business Disruption business disruption: • Conduct a business impact analysis so you understand the potential consequences of the risks you are self-insuring as well as the mitigation and recovery strategies needed to support resilience. Your broker should be able to advise you on how to approach this analysis. • Check your business interruption (BI) policy. A typical 12-month policy may not be sufÏcient to bridge the time between loss and reconstruction, as evidenced by the 2024 wildfires in Jasper, Canada, which destroyed a third of the community. A 24-to-36-month BI policy is becoming a more realistic option to support a full recovery from a catastrophic event. • Lean on your broker for real-time guidance driven by best-in-class artificial intelligence tools when the supply chain is impacted by a disaster. While the immediate location impacted may be inoperable to produce goods or services, a broker who has a dynamic inventory solution can pivot on the fly to minimize further reaching consequences, including making changes to current policies. • Have a “people plan” in place to help support employees in the event of a disaster. The plan should focus on establishing communication with employees using tools such as bi-directional texting to help them access their medical, pharmacy and EAP benefits. If the company ofÏce or facility is not impacted, consider offering food, showers, refrigeration storage and parking, where available. • Annually update replacement costs in property insurance policies to keep pace with rising costs and property values and develop a multi-year plan to keep up with building maintenance. 2. Verisk, “New Report: Average Annual Natural Catastrophe Losses for the Insurance Industry Reaches New High of $151 Billion,” September 3, 2024 3. Forbes, “Climate Damage To Hit $38trn - The Economy Needs Action Now,” April 22, 2024 9 | HUB Int9 | HUB Internaernational 2025 North American Outlook Rtional 2025 North American Outlook Reporteport

Growing Cyber Risks Amid a Staggering Lack of Preparedness Companies are waking up to the devastating financial losses associated with funds transfer fraud, invoice manipulation, social engineering, ransomware and deepfake attacks. The projected global cost of deepfake fraud in 2024 is anticipated to reach $1 trillion, 4 presenting a substantial threat to markets and the global economy. In last year’s HUB survey, respondents ranked their cyber risk as relatively low. In 2024, they identified it as a higher risk but one that they are adequately prepared to handle. However, the HUB survey indicates no discernable increase in cyber insurance coverage year over year with only 40% of respondents reporting that they have some form of cyber coverage. There is plenty of capacity available in the cyber insurance market and securing coverage is a critical component to recover from a cyberattack. Cyber policies have evolved significantly and cover a wide range of risks but require organizations to have robust policies and procedures and comply with regulatory requirements. How Your Broker Can Help: Cyber Insurance How Your Broker Can Help: Cyber Insurance • Get insights into the health of your cyber security program with a Bitsight Security Rating, an objective, data-driven lens that identifies exposures and hidden risks. The rating is also used by insurance carriers to underwrite policies. • Use advanced cyber benchmarking tools to help determine the appropriate limits needed. TM SCORE (Stochastic Cost of Risk Evaluation) modeling is also available for companies with more complex cyber risks. • Evaluate your organization’s exposure by considering important factors such as how much customer data your organization retains, your record retention policies and frequency of cyber security training for employees. • Offer cyber protection to employees to help them protect their identity and devices and make it harder for hackers to steal personal information, not to mention company information for those who work remotely. Recovering from identity theft is time-consuming and can adversely impact employee productivity. 4. Security Intelligence, “How a new wave of deepfake-driven cyber crime targets businesses,” May 17, 2024 HUB International 2025 North American Outlook Report | 10

SUCCESS STORY: Rising from the Ashes A performing arts school (and not a HUB client at the time of loss) suffered a major fire that destroyed its performance venue and greatly disrupted operations. To rebuild, they applied for a multimillion-dollar grant from a private donor, who required them to demonstrate their enhanced resilience as a condition of the grant. They engaged HUB to assess their existing crisis management and continuity plans. The enhanced program was submitted to the donor, resulting in the release of an initial $2.5 million transfer of grant funds. The school is now better equipped to prepare for and recover from a disruptive event in the future. SUCCESS STORY: Cyber Insurance Provides a Quick Recovery A nonprofit that specializes in working with at-risk youth reached out to HUB fearing it was under a ransomware attack, exposing vulnerable patient and resident data. HUB immediately put an action plan into place to minimize access to emails and other sensitive information. After bringing in forensic accountants, it was determined there was no data stolen during the event. The client was not only relieved that the impact was minimal and resulted in a total claim under $60,000, but the organization also took the opportunity to train its staff to be better prepared in the future. 11 | HUB International 2025 North American Outlook Report

Geopolitical Risks are Right in Your Backyard Geopolitical instability has the potential to be a major disruptor, yet survey respondents don’t appear to see the connection between it and the risks they are tracking closer to home. Only 21% of respondents The fact is what indicated geopolitical risks as likely to affect their company's profitability in 2025. happens “over there” has a lot to do with what happens here, namely increased costs from supply chain disruptions and cyberattacks that originate from overseas, as well as domestic legislative and regulatory changes in response to global threats. Clients should also consider having backup or contingency plans in place to help mitigate losses or disruptions due to supply chain issues. How Your Broker Can Help: Geopolitical Risk How Your Brokers Can Help: Geopolitical Risk • Political risk insurance (PRI) helps businesses manage risks arising from political violence, contract frustration, sovereign payment default or government actions, such as confiscation, expropriation or currency inconvertibility, as well as nonpayment by foreign governments on cross-border loans or contracts. • Trade credit insurance will help protect balance sheets. How Your Broker Can Help: International Expansion • Assist in conducting a risk analysis of the local infrastructure in a region before investing. • Consult with insurance partners in the region who have been carefully vetted for their expertise. • Clarify locally admitted, required and mandatory insurance policies needed. • Secure political risk insurance. HUB International 2025 North American Outlook Report | 12

SUCCESS STORY: Managing the Risk of International Expansion A technology company experiencing rapid expansion overseas suspected that its insurance program and regulatory compliance were not keeping pace with its current and planned growth. The company engaged with HUB which conducted a global optimization review that identified coverage redundancies and coverage gaps between the local and master global policies. As a result, the global program was redesigned, and local policies were adjusted, resulting in cost savings and enhanced compliance. HUB also improved global broker network communication and provided company executives a “Global Insurance 101” training with a contract review playbook, thereby giving them the information they needed to make informed decisions when managing their overseas operations. SUCCESS STORY: Taking Analytics Beyond Benchmarking A large construction company wanted to better understand how to structure its commercial insurance program. HUB reviewed the company financials and loss history and conducted a TM TM SCORE report, using stochastic modeling. The data and insights gained from the SCORE report, which is available on 13 lines of coverage, were specific to the client and their financial situation. As a result, the client was able to better understand its options regarding its current deductible retention and make informed decisions about its risk-bearing capacity at its next renewal. 13 | HUB International 2025 North American Outlook Report

Rely on Insurance to Protect the Bottom Line The cost and availability of insurance is under pressure across many industries and geographies. According to the HUB survey, economic challenges and inflation have significantly to moderately affected 81% of companies' ability to secure ample insurance coverage. 73% of companies report being underinsured 39% of companies describe analytics as against profit-threatening risks, a slight extremely important and 27% regard it as improvement from 76% in 2023. Commercial significantly important to the structuring and coverage for property, general liability financing of property insurance. and umbrella insurance has all decreased compared to 2023. 96% of respondents do not have a formal process to identify and derive their annually 63% describe their property insurance as a reported property values and exposures. traditional model with coverage provided by a single carrier per line of business. How Your Broker Can Help: Risk Transfer Strategy The risk exposure facing businesses across North America is substantial and without adequate insurance, the risk of bankruptcy is high. Here’s how your insurance broker can help. • Make sure your insurance broker thoroughly understands your business model, your company’s challenges and goals before recommending coverage. Don’t treat insurance like a transaction or a procurement exercise. • Use benchmarking and stochastic modeling to shape the structure and financing of your property insurance. While benchmarking continues to be valuable, there’s been a massive acceleration in the use of analytics that helps companies manage costs and “see around the corner.” • Your insurance broker should have a demonstrated track record in helping companies reduce losses and claims. Underwriters give preferential treatment to brokers who have lower than average loss ratios on their book of business because it signals a commitment to risk management. • Alternative approaches to traditional insurance might be a viable option. Based on historical losses, you may be able to save money by combining property and casualty coverage on an excess policy. Or you may secure a multi-year insurance program where a percentage of premiums are returned if losses are better than anticipated. Another option is insurance programs that require a letter of credit. • Identify the assets and the emerging risks that cannot be covered and lean into enterprise risk management to mitigate it. HUB International 2025 North American Outlook Report | 14

Workforce Vitality Human Resources Leaders Grapple with Employee Productivity and Rising Costs According to the HUB International 2025 Outlook Executive Survey, companies that responded say their top priorities for 2025 are (in order of importance): employee productivity, cost of medical benefits, cost of pharmacy drugs, employee compensation and AI. Improve employee productivity — 66% of U.S. and 75% of Canadian firms identify employee productivity as a key focus for 2025, with most planning to align total rewards, specifically compensation, with productivity metrics. The reasons for the prioritization of employee productivity are varied and include creating value through improved efÏciency, achieving a competitive advantage and aligning with C-suite goals. Productivity can be measured in a variety of ways, including revenue, sales growth, production volume, enrollment in programs, clients served and performance ratings. Annual incentive plans generally include multiple measures of productivity. Today’s HR leaders are building human-centric workplaces. They recognize that appropriate compensation is a baseline requirement for retaining talent, but it’s not enough to build a high- performing workplace. Human-centric environments are built on multiple pillars, such as wellbeing, flexibility, social connection, continuous learning, recognition and effective communication, among others. Together, they foster a culture of trust, collaboration and innovation and lead to higher levels of employee engagement. Reduce the overall cost of medical benefits — 67% of U.S. and Canadian firms plan to reduce the cost of medical benefits in 2025, with most U.S. firms focusing on making HR policy changes (41%) and Canadian firms focusing on major plan changes (40%). • HR policy changes can include such tried-and-true cost-savings measures as increasing premiums for smokers, charging more for spousal coverage or removing spouses if they can get health benefits through their employer. • 61% of survey respondents are reducing operational costs to maintain their employee benefits. Employers can also reduce costs through managing health and employee wellbeing. Studies have shown that the ROI for wellness programs is about $1.50 to $3 less in medical claims for every dollar spent. hubinternational.com 15 | HUB International 2025 North American Outlook Report

Just as urgent, employers need to leverage data analytics, clinical informatics and claims data to better identify health risk trends and analyze contracts with providers, resulting in savings not visible on the surface. This type of analysis is at the forefront of cutting costs — especially pharmaceutical expenses. Reduce the overall cost of pharmacy benefits — Prescription drug costs are growing at nearly twice the rate of overall health benefit costs, driven largely by specialty drugs. Gene therapy and weight loss drugs, for example, can cost organizations millions, if not actively managed. According to the HUB survey, 39% of U.S. firms plan to address rising pharmacy drug costs by re- evaluating their consultant/broker relationship. U.S. firms may be feeling some pressure in response to recent lawsuits filed against employers for failure to protect the interests of employees and families enrolled in Rx plans administered by a Pharmacy Benefit Manager (PBM). Re-evaluating PBM contracts is one way to reduce potential liability. Q Which of the following issues are a key priority for 2025 that your company needs to address? N=910 69% 67% 59% 49% 36% 80 90 100 Companies that have assigned a high priority to AI intend to use it to achieve cost savings through operational efÏciencies or staff reductions. Those prioritizing AI recognize there are legal and compliance concerns that must be addressed with over half of them planning to revise their HR policies in 2025 (55% of U.S. and 54% of Canadian firms). HUB International 2025 North American Outlook Report | 16

Solutions to Address Employee Financial Stress Given their prioritization of employee productivity, survey respondents are also concerned about employee financial stress and are taking steps to support their workforce. Employees report a loss of more than seven hours of productivity per week due to financial stress, amounting to an annual cost of $183 billion for U.S. employers.5 Inflation has taken a toll on both short-term and long-term savings. • A record-high 3.6% of participants took hardship withdrawals from their 401(k), up from 6 2.8% in 2022. This increase has been attributed to inflation, rising interest rates and changing rules that make it easier for people to access these funds. • Home insurance rates rose an average of 11.3% in 2023 due to severe weather, inflation 7 and rising homebuilding costs. The most expensive states for home insurance are Florida 8 ($11,759), Louisiana ($7,809) and Oklahoma ($5,711). 9 • Rising auto insurance premiums have impacted 67% of Americans. According to our survey, companies in both the U.S. and Canada are trying to reduce employee financial stress by offering personal insurance coverage options. • 78% of middle market firms and 74% of upper middle market firms are considering offering personal insurance coverage options in 2025. • Currently, 22% of business leaders are offering auto/home/personal insurance solutions to employees. Companies across various industries are also actively taking steps to boost retirement plan participation. According to our survey, the primary areas of focus are: • Requesting additional support from retirement plan providers (37% in the U.S., 38% in Canada). • Provide counseling to help employees understand their retirement plan (39% in Canada). 5. BrightPlan, “New Study: 86% of Gen Z Workers are Stressed About Their Finances Reporting Over 8 hours a Week in Lost Productivity, “ April 30, 2024 6. Vanguard, “How Americans withstand financial hardships,” September 19, 2023 7. S&P Global, “US homeowners insurance rates jump by double digits in 2023," January 25, 2024 8. Insurify, “Average Cost of Home Insurance (October 2024),”Accessed November 3, 2024 9. Prudential/Assurance IQ, “Study: Home and auto insurance cost increases stretch Americans’ budgets,” October 5, 2023 17 | HUB International 2025 North American Outlook Report

SUCCESS STORY: Designing Compensation Plans That Boost Performance A children's home in South Dakota understands the important role its employees play in empowering people and helping prevent, treat and heal those who are recovering from trauma. They wanted to offer competitive and equitable compensation to help attract, reward and retain talent. With HUB’s help, they developed a new employee compensation strategy, established job benchmarks and built and implemented a market-based, best practice pay program that rewards employees for performance, a key measure of productivity, and for years of service. SUCCESS STORY: Choosing Custom Over Default Formulary Wins A talent recruitment agency in Canada recognized that to be a leader in its industry, it had to demonstrate leadership in the health benefits it offered its own employees. Working with HUB, the agency developed its own formulary in conjunction with a third-party provider that reduced costs while meeting the needs of its employees. Plan sponsors should compare the value of choosing their own drug formulary over accepting the default formulary offered. SUCCESS STORY: Offering Personal Insurance to Ease Employee Financial Stress An organization with a workforce of more than 12,000 employees partnered with VIU by HUB to offer personal insurance options. Given the size and complexity of the organization, providing scalable yet tailored insurance was essential to meet the diverse needs of its employees. Accessing an omnichannel platform, 14% of eligible employees explored personal insurance quotes and more than 7% went on to become customers. Auto insurance was the most popular product, representing 50% of policies purchased, followed by tenant insurance at 23%. This collaboration demonstrates the value of VIU by HUB’s digital-first approach to insurance, making it easier for employees to find coverage that fits their individual needs and enhancing the organization’s overall benefits offering. HUB International 2025 North American Outlook Report | 18

How Your Advisor Can Help: Financial Wellness How Your Advisor Can Help: Financial Wellness • Provide digital, self-service tools that guide users through a series of goals such as how to establish emergency savings funds, improve credit score, lower debt, buy a home and prepare for retirement. • Provide access to certified financial coaches who do not work on commission and offer unbiased advice to employees. SUCCESS STORY: Using Retirement Benefit Matches to Boost Productivity and Retention School districts in both urban and rural areas are using retirement plan matches and vesting schedules to incentivize recruitment, retention and attendance. These extra incentives are deployed in areas where recruitment and retention are a challenge or to reduce the costs associated with hiring substitute teachers. To help boost employee productivity, HUB worked with school districts to establish an attendance benchmark based on historical data and the additional match to be offered above the retirement plan base match. Teachers who achieve the benchmark during the school year receive the higher employer match. Clients who implement the higher match in conjunction with automatic enrollment have seen plan participation increase from 35% to 95%. 19 | HUB International 2025 North American Outlook Report

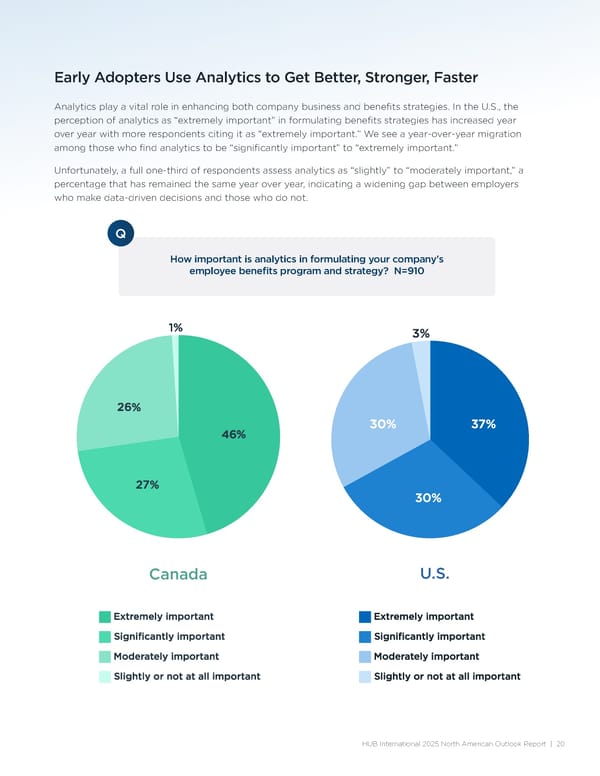

Early Adopters Use Analytics to Get Better, Stronger, Faster Analytics play a vital role in enhancing both company business and benefits strategies. In the U.S., the perception of analytics as “extremely important” in formulating benefits strategies has increased year over year with more respondents citing it as “extremely important.” We see a year-over-year migration among those who find analytics to be “significantly important” to “extremely important.” Unfortunately, a full one-third of respondents assess analytics as “slightly” to “moderately important,” a percentage that has remained the same year over year, indicating a widening gap between employers who make data-driven decisions and those who do not. Q How important is analytics in formulating your company's employee benefits program and strategy? N=910 Canada U.S. HUB International 2025 North American Outlook Report | 20

Those companies that are committed to data-driven decision-making report using analytics to improve individual outcomes, streamline costs and understand claims trends. Early adopters also used analytics, like HUB Workforce Persona Analysis, to analyze their workforce demographics and tailor benefits to meet the unique needs of multiple generations. How Your Broker Can Help: Analytics Organizations that are already leveraging analytics will be best positioned to take advantage of these new capabilities. Here’s a few examples of what the future state of analytics holds. • Combining disparate data sets from medical and retirement benefits to better understand employee financial stress and offering resources to support individual needs. • Incorporating data from employee questionnaires to identify financial stressors (i.e., student loan debt and caregiver responsibilities). • Measuring and driving engagement. • Predicting future trends and impacts on benefits plan. 21 | HUB International 2025 North American Outlook Report

Resiliency Getting Ready for the Next Major Disruption First, the good news: 62% of respondents indicated that their companies have adopted a formal enterprise risk management (ERM) assessment process. Their primary focus is disaster planning, followed by calculating risk-bearing capacity and tolerance levels and reviewing risk protocols and procedures. Now, for the blind spots. Of the companies that said they have a formal ERM, only 22% of U.S. companies include political risk and only 21% of Canadian companies include business interruption in their ERM exercises. Given today’s environment, all companies need to be ready for the next business disruption, be it political, social or weather-related. Many firms underestimate the devastating impact that geopolitical instability can have on their supply chain. ERM: No Longer Just a “Nice-to-Have" Enterprise risk management (ERM) is a critical tool for addressing today’s rapidly evolving risks. It provides a 360-degree view of a company’s individual risk landscape, breaking down silos and ensuring that everyone, from C-suite to the front line, is aligned on managing risk. 62% of companies surveyed have a formal enterprise risk management (ERM) 10 assessment process. In the 2024 survey, both monthly and annual ERM assessments increased in frequency across multiple industries compared to 2023 survey results. Middle market companies are increasingly conducting ERM assessments monthly or quarterly as compared to 2023, while upper middle market companies moved toward less frequent evaluations in 2024. The increase in frequency among middle market companies may be due to concerns about evolving risk exposures or a problem with the assessment method itself. When embedded into a company’s culture and supported by leadership, ERM ensures that risks are managed before they escalate. 10. HUB International 2025 Outlook Executive Survey 22 | HUB International 2025 North American Outlook Report

When it comes to ERM, HUB recommends the following: How Your Broker Can Help: ERM • Conduct an annual enterprise-level assessment with divisional or business unit assessments on a rolling calendar throughout the year so all segments of the organization are addressed every 18 to 24 months. • Initiate a new review of the current ERM strategy if a major change occurs in the organization, such as new leadership, expansion or a shift in market dynamics. • Plan for the consequences of a disruptive event, not just the event itself, and have contingency plans for protecting people, facilities, supply chains and operations. • To succeed, ERM exercises must be streamlined and fit the company culture. SUCCESS STORY: Using ERM and Insurance to Prepare for the Worst A grain grower in Canada engaged with HUB specialists to conduct an ERM assessment that enabled it to catalog and prepare for almost 60 enterprise-level risks. It was determined that the most severe risk to the business was a major drought that could substantially decrease the grower’s yield. A multi-year parametric hedge was structured that would respond when a drought of specified severity was experienced. In the second year of the policy, the client— along with its competitors—experienced a severe and prolonged drought that threatened the industry. The hedge policy was triggered and paid in full, thereby enabling the business to maintain its target financial strength. Later that year, it acquired a larger competitor. HUB International 2025 North American Outlook Report | 23

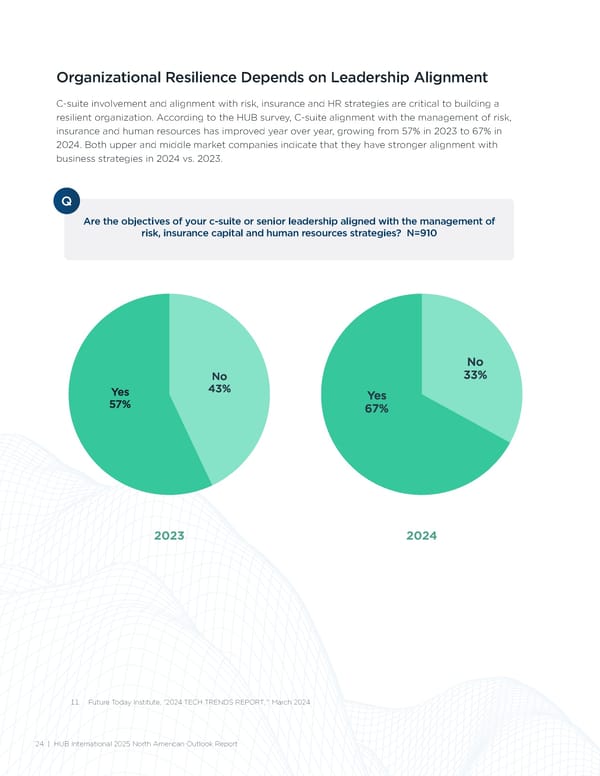

Organizational Resilience Depends on Leadership Alignment C-suite involvement and alignment with risk, insurance and HR strategies are critical to building a resilient organization. According to the HUB survey, C-suite alignment with the management of risk, insurance and human resources has improved year over year, growing from 57% in 2023 to 67% in 2024. Both upper and middle market companies indicate that they have stronger alignment with business strategies in 2024 vs. 2023. Q Are the objectives of your c-suite or senior leadership aligned with the management of risk, insurance capital and human resources strategies? N=910 2023 2024 11. Future Today Institute, ”2024 TECH TRENDS REPORT," March 2024 24 | HUB International 2025 North American Outlook Report

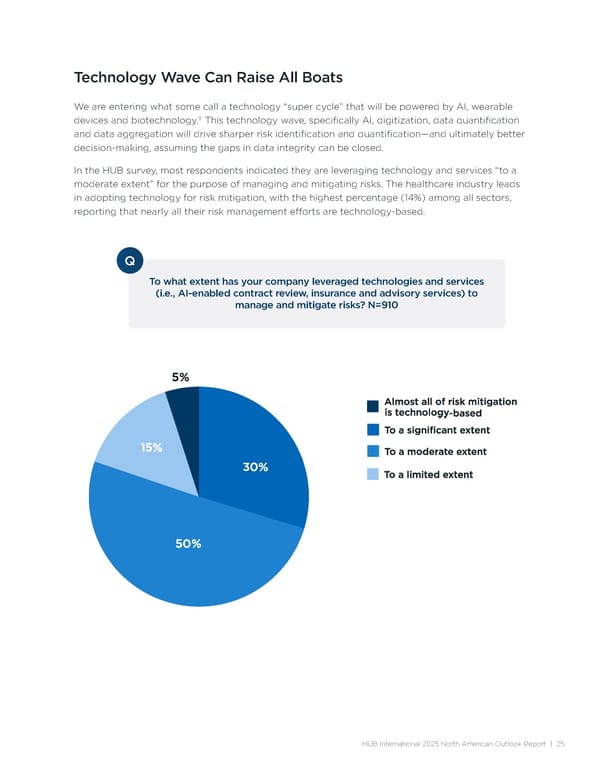

Technology Wave Can Raise All Boats We are entering what some call a technology “super cycle” that will be powered by AI, wearable 11 devices and biotechnology. This technology wave, specifically AI, digitization, data quantification and data aggregation will drive sharper risk identification and quantification—and ultimately better decision-making, assuming the gaps in data integrity can be closed. In the HUB survey, most respondents indicated they are leveraging technology and services “to a moderate extent” for the purpose of managing and mitigating risks. The healthcare industry leads in adopting technology for risk mitigation, with the highest percentage (14%) among all sectors, reporting that nearly all their risk management efforts are technology-based. Q To what extent has your company leveraged technologies and services (i.e., AI-enabled contract review, insurance and advisory services) to manage and mitigate risks? N=910 HUB International 2025 North American Outlook Report | 25

Conclusion Can Disruption Create New Opportunities? Turning disruption into opportunity only exists for organizations with a comprehensive and mature risk management program. It takes a seasoned driver to navigate disruption and move into a new lane that opens. 26 | HUB International 2025 North American Outlook Report

Based on the HUB 2025 Outlook Executive Survey findings, here are the key actions that organizations need to take together with their insurance broker and benefits advisor to prepare for what comes next: • Align business goals with risk strategies. It starts with alignment across C-suite, risk and human resources leadership moving together to build a total view of risk vs. siloed response. Alignment is fundamental to eliminating blind spots. • Invest in advanced data analytics to not only understand risk but to also understand and address employees' needs. • Amplify the focus on employee wellbeing to enhance workforce vitality. • Recognize that compensation is a baseline requirement for retaining talent. Building a high-performing workplace requires multiple pillars that support employees’ physical, emotional and mental health. • Have a clear vision for the future but be agile on how to get there. Lastly, consider the key partners you need to achieve your growth, resiliency and workplace vitality goals. With the help of an expert insurance broker, risk consultant and benefits advisor, you can take your organization to the next level and win big in 2025 and beyond. HUB International 2025 North American Outlook Report | 27 HUB International 2025 North American Outlook Report | 27

Lean In. Seek Opportunity. Win Big. Table of Contents The risk landscape in 2025 will be increasingly volatile and complex. New risks are emerging faster than ever and organizations that are preparing now will be ready to embrace Executive Summary and Key Insights 4 the future and win big. Profitability: Both New and Familiar Risks 8 Now is the time to protect your organization and people. Threaten Company Profits Align your organizational goals to your risk, insurance and benefits strategies. Workforce Vitality: Human Resources Leaders Grapple with 16 Employee Productivity and Rising Costs Consider the partners you may need to engage to ensure you are taking the right steps to protect your profits, cultivate a vital Resiliency: Getting Ready for the Next Major Disruption 24 workforce and create a more resilient tomorrow. For additional insights, explore our industry and sector-specific Conclusion: Can Disruption Create New Opportunities? 28 U.S. and Canadian reports. 28 | HUB International 2025 North American Outlook Report

About HUB When you partner with HUB, you're at the center of a vast network of experts who will help you improve your profitability, enhance the vitality of your workforce and remain resilient into the future. For more information on how to manage your insurance costs, reduce your risk and take care of your employees, talk to your HUB advisor or visit hubinternational.com. We're here to help. 5th 540+ 18,000+ largest insurance locations across employees broker in the world North America hubinternational.com The information in this piece is solely for general information purposes and is not intended as tax or legal advice. We do not warrant the accuracy, completeness or usefulness of the information. We disclaim all liability and responsibility arising from any reliance placed on the information by you or anyone else who may be informed of any of its contents. This information may include content provided by other parties. All statements and/or opinions expressed in these materials, other than the content provided by HUB, are solely the opinions and the responsibility of those other parties and do not necessarily reflect the opinion of HUB. We are not responsible or liable for the content or accuracy of any materials provided by any other parties. 3030 HUB International North America 2025 Outlook Report | 30